Complementary Law (CL) No. 227/2026 represents another relevant step in the implementation of Brazil’s Consumption Tax Reform. The law regulates the organization, powers, and operation of the IBS Management Committee (CGIBS), which will coordinate the collection, oversight, revenue allocation, and uniform interpretation of the new Goods and Services Tax (IBS).

The law also introduces national guidelines for the Inheritance and Donation Tax (ITCMD), aiming to harmonize state rules on taxable events, connecting factors, and taxing authority, particularly in cases involving foreign assets, cross-border donations, and estates with links to multiple jurisdictions.

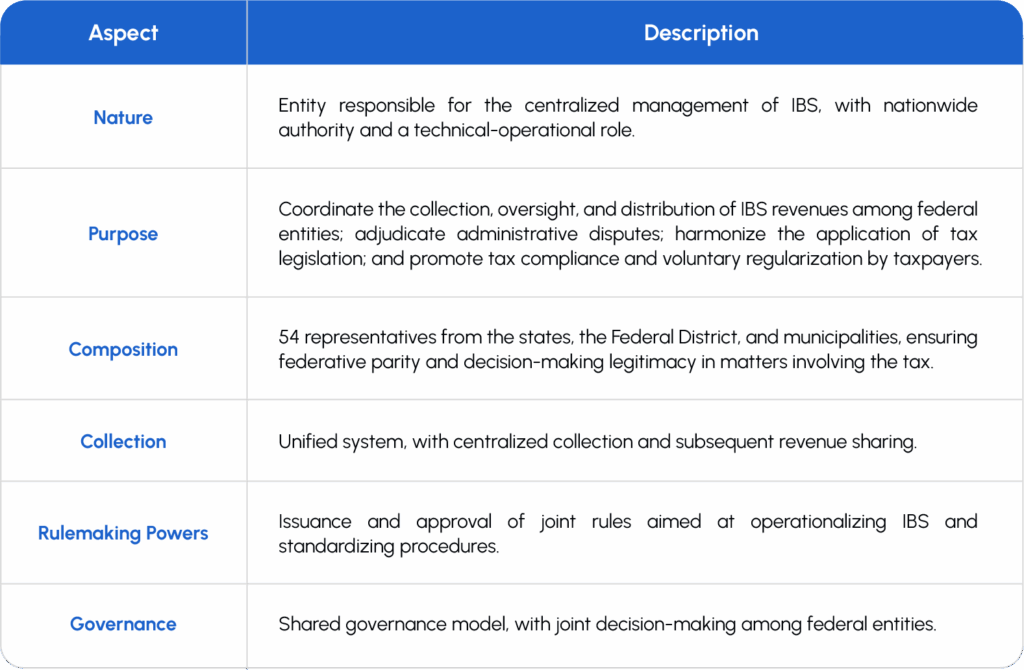

IBS Management Committee

From a practical standpoint, the CGIBS will play a strategic role in implementing the new tax system. Its functions include managing the unified collection system, defining ancillary obligations, and implementing mechanisms for credit compensation and revenue sharing among states and municipalities.

This centralization may reduce the complexity of the current tax system, but it will also require companies to closely review their internal processes and tax systems.

IBS Management Committee (CGIBS) – Key Features

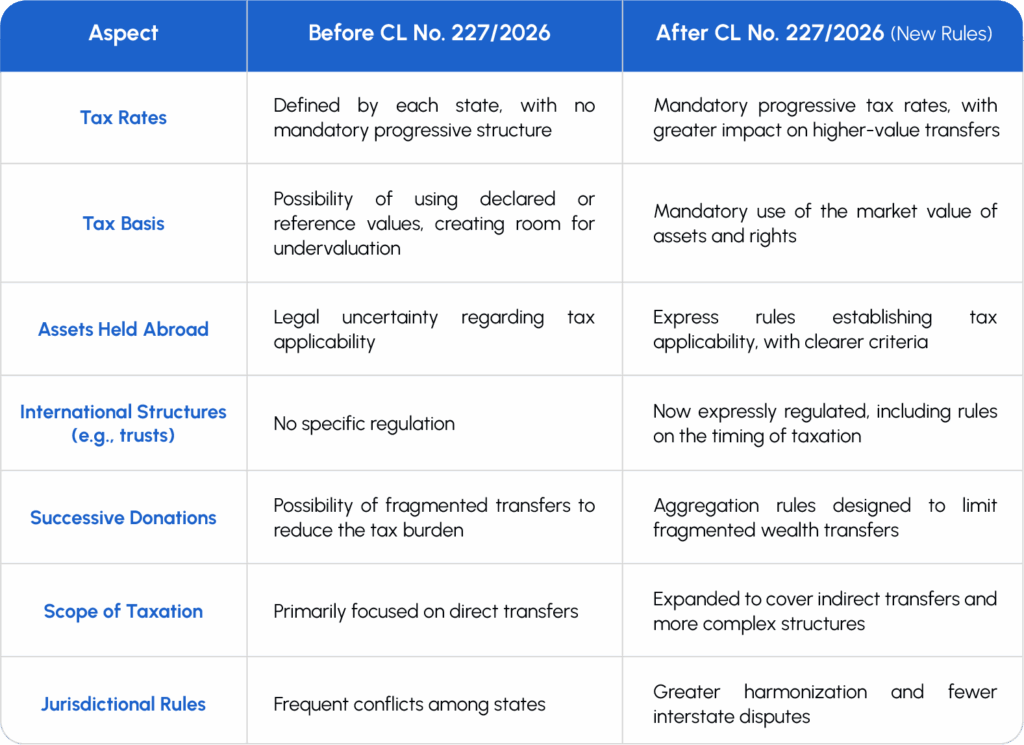

ITCMD – Key Changes

With respect to ITCMD, CL No. 227/2026 sets national guidelines designed to reduce interpretive conflicts among states and provide greater certainty in wealth transfer taxation.

Among the most relevant changes is the adoption of market value as the tax basis, which changes how transferred assets and rights are measured. This may increase the effective tax burden and reduce the use of planning structures based on undervalued assets.

The law also requires progressive tax rates, which may result in a heavier tax burden, especially for transfers involving higher-value assets.

In addition, the law provides greater clarity on the taxation of assets held abroad, an issue historically marked by disputes and litigation. By setting general parameters, the new rules may improve predictability in estate and succession planning, including family holding structures.

Recommended Next Steps

Companies, families, and investors affected by CL No. 227/2026 should:

- Review corporate structures and estate planning arrangements

- Assess the impact of market value rules on assets and rights

- Revisit family holding structures involving Brazilian or foreign assets

- Review internal tax routines in light of the CGIBS framework

- Monitor state-level implementation of the new ITCMD guidelines

The changes introduced by CL No. 227/2026 require a careful review of corporate structures, succession planning, and corporate tax routines. The operation of the CGIBS and the harmonization of ITCMD rules are expected to reduce tax arbitrage opportunities while increasing the need for tax compliance and governance.