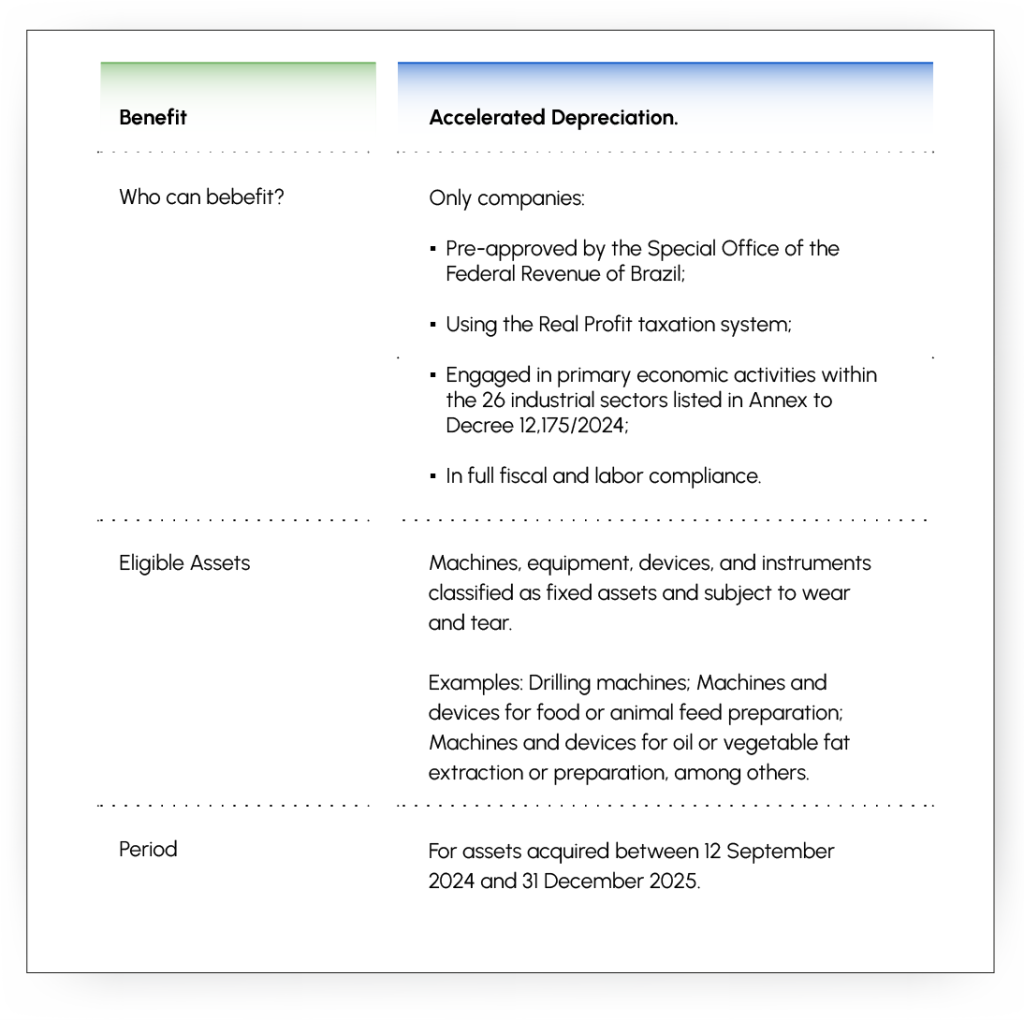

On 11 September 2024, the Executive Branch issued Decree 12,175. It regulates the effects of granting accelerated depreciation rates for new machinery, equipment, devices, and instruments, as provided under Law 14,871 of 28 May 2024. These assets must be allocated to fixed assets and used in specific economic activities.

These rules aim to boost productivity by encouraging the acquisition of energy-efficient and modern machinery. This approach seeks to modernize Brazil’s industrial infrastructure.

The accelerated depreciation benefit applies to companies operating within a group of 26 industrial sectors, provided they are in full tax compliance and adopt the Real Profit taxation system, a method where corporate income tax is calculated based on net profits adjusted for additions and exclusions as defined by law. This incentive allows companies to deduct 50% of the asset’s value in the year it is installed, operationalized, or ready for production, with the remaining 50% deducted in the following year. By granting accelerated depreciation rates for new fixed assets employed in specific economic activities, this benefit offers immediate tax savings in the initial years of asset use, positively impacting their operating cash flow.

A list published by the Executive Branch specifies which machines, devices, and instruments qualify for differentiated accelerated depreciation. Buildings, structures, and similar items are excluded from this benefit.

Furthermore, subsequent additions of accounting depreciation can be fully offset against accumulated tax losses. Notably, the general 30% cap on compensation for tax adjustments does not apply in this case, ensuring a more substantial cash flow gain for companies.

The accelerated depreciation benefit provided under Law 14,871/2024 is available exclusively for the acquisition of capital goods purchased between 12 September 2024 and 31 December 2025. Companies should act quickly to leverage this opportunity to optimize their tax benefits and improve cash flow.

Glossary:

Law 14,871/2024 – Brazilian legislation establishing accelerated depreciation rates for specific assets to encourage industrial modernization and energy efficiency.

Decree 12,175/2024 – the regulation detailing the application and conditions for the accelerated depreciation benefit introduced by Law 14,871/2024.

Fixed Assets – long-term assets, such as machinery and equipment, used in a company’s operations and not intended for resale.

Real Profit Taxation System – a corporate taxation model in Brazil where taxes are calculated based on the company’s net profits, adjusted for specific inclusions and exclusions as defined by law.

Selic Rate – Brazil’s benchmark interest rate, set by the Central Bank, used to calculate monetary adjustments and penalties.

Tax Adjustment Cap – a 30% limit in Brazil on using accumulated tax losses to offset taxable income, not applicable to the accelerated depreciation under Law 14,871/2024.