A recent Complementary Law introduces a 10% reduction across various federal tax incentives, effective as of 2026. The legislation also restricts the attractiveness of the presumed profit regime for larger companies, increases taxation on Interest on Net Equity (JCP), and imposes structural constraints on the future expansion of tax benefits, resulting in a significantly higher effective tax burden for most taxpayers.

Scope of the 10% Reduction

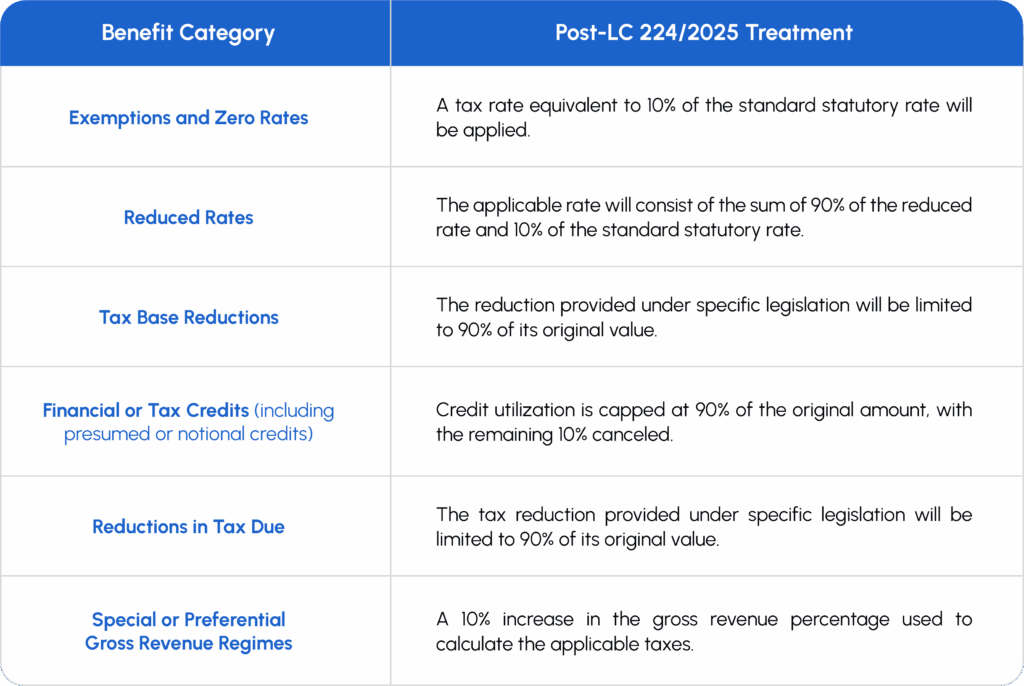

The mandatory 10% cut applies to a broad range of federal tax benefits, specifically targeting:

- Incentives related to the Social Integration Program (PIS), the Contribution for the Financing of Social Security (COFINS), Corporate Income Tax (IRPJ), Social Contribution on Net Income (CSLL), Excise Tax (IPI), Import Tax, and employer social security contributions.

- All tax benefits and incentives listed in the Tax Expenditure Statement attached to the 2026 Annual Budget Law.

- The presumed profit regime and presumed IPI tax credits.

Statutory Exemptions

The reduction applies universally, subject only to strict exceptions expressly provided in the legislation, which include:

- Constitutional tax immunities.

- The Manaus Free Trade Zone.

- The National Essential Food Kit.

The 10% reduction applies according to the category of each tax benefit, as follows:

Analysis of Structural Changes

- Sectoral Impact:The 10% reduction directly targets the mechanisms used to mitigate taxes on revenue, profit, and production. This creates a disproportionate impact on sectors that rely heavily on tax incentives for their operational viability.

- New Fiscal Thresholds:Future tax benefits are now subject to strict GDP-based thresholds for their creation, expansion, or extension. If total tax expenditures exceed 2% of GDP, new concessions or extensions are prohibited without compensatory measures – signaling a structurally more restrictive environment for tax incentives in the medium term.

- Corporate & Remuneration Shifts:

- The presumed profit regime is now less advantageous for companies with annual gross revenue exceeding BRL 5 million, necessitating a reassessment of its efficiency compared to the actual profit regime.

- The increase in withholding tax (IRRF) on Interest on Net Equity (JCP) from 15% to 17.5% further diminishes its effectiveness as a shareholder remuneration tool.

Effective Dates

- Corporate Income Tax (IRPJ): 1 January 2026.

- All Other Taxes: 1 April 2026.

Practical Impact

LC 224/2025 reshapes the economic logic of tax incentives in Brazil, moving beyond a simple technical adjustment to a structural increase in the effective tax burden. This new landscape demands immediate, data-driven decisions. Organizations must prioritize a comprehensive reassessment of their tax, financial, and operational models to preserve margins and ensure long-term financial predictability.

Glossary:

Presumed Profit Regime – A Simplified Corporate Tax Regime Based On Presumed Margins

Interest On Net Equity (JCP) – A Brazilian Profit Distribution Mechanism With Tax Consequences

Tax Expenditure Statement – The Government’s Official List Of Tax Expenditures/Incentives

Annual Budget Law – The Statute Approving The Annual Federal Budget

Social Integration Program (PIS) – A Federal Contribution Levied On Revenue (Acronym Used In Brazil)

Contribution For The Financing Of Social Security (COFINS) – A Federal Contribution Levied On Revenue (Acronym Used In Brazil)

Corporate Income Tax (IRPJ) – Brazil’s Corporate Income Tax (Acronym Used In Brazil)

Social Contribution On Net Income (CSLL) – Brazil’s Social Contribution On Net Income (Acronym Used In Brazil)

Excise Tax (IPI) – A Federal Tax On Manufactured Products

Import Tax – A Federal Tax Levied On Imports

Employer Social Security Contributions – Mandatory Payroll-Related Contributions Paid By Employers

Presumed IPI Tax Credits – Deemed Credits Granted By Statute, Not Based On Actual Tax Paid

Manaus Free Trade Zone – A Special Tax Regime For The Manaus Region

National Essential Food Kit – A Tax-Policy Category Covering Essential Food Items

Standard Statutory Rate – The Normal Legal Rate Applicable Absent An Incentive

Notional Credits – Credits Created By Statute Without A Cash Outlay

Withholding Tax (IRRF) – Tax Withheld At Source Under Brazilian Rules

Actual Profit Regime – The Standard Corporate Regime Based On Actual Taxable Profit